7 Critical Factors Women Entrepreneurs Must Be Mindful of When Procuring Business Loans

- 40% of MSMEs in India are women-led

- Access to formal credit is crucial, but business success depends on smart financial planning, strategic loan utilization, and responsible debt management

- Entrepreneurs must navigate various factors that influence loan approval and terms—loan-to-value assessments, credit scores, processing times, and documentation

- Personal and business finances must be separate, with realistic growth projections

- Actively negotiating loan terms can secure the best financial support for the business journey

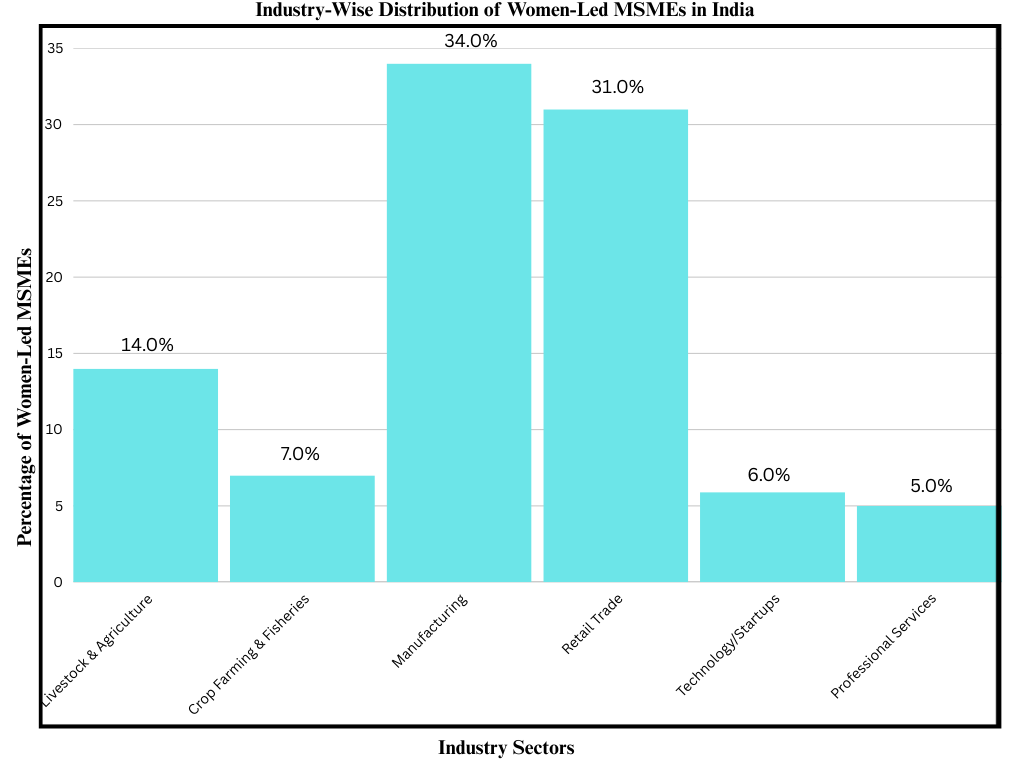

Approximately 40% of MSMEs in India are women-owned, with a strong representation of 34% in manufacturing and 31% in retail trade. Policy incentives, digital transformation, and shifting cultural dynamics have led to this surge, shaping India’s inclusive economic growth.

Access to formal credit is among the most crucial contributors in accelerating this momentum of growth and sustainability. And to procure and utilize funds optimally, entrepreneurs must have a well-structured business plan, sound financial management, and informed decision-making.

This article serves as a practical guide for women entrepreneurs, offering actionable insights to navigate the business loan procurement process and take confident steps toward financial empowerment and sustainable growth.

Understanding Business Loans

Business loans serve multiple purposes for small businesses. While many entrepreneurs view loans with concern, they can actually provide critical support for small and medium enterprises. Furthermore, business loans offer more than just immediate financial relief – they help solve working capital challenges, fuel expansion plans, strengthen financial stability, and create opportunities to scale operations.

The key lies not in just obtaining a loan, but in transforming it into a growth opportunity. Smart financial planning should consider both the loan’s immediate use and a comprehensive repayment strategy. The loan should be used wisely and repayments managed carefully.

How to prepare for a business loan

Preparing for a business loan requires careful groundwork. It should begin by developing a clear business plan that outlines specific goals, financial requirements, and growth projections. Lenders want to see a roadmap that demonstrates your business’s potential and your strategic thinking. This means gathering all important and necessary documentation that builds the business’s credibility.

A well-prepared application focuses on the following 5 factors:

- Clear Objectives & Vision: A well-defined objective and vision serve as the foundation for strategic growth, outlining both short- and long-term goals. Clearly specifying loan utilization ensures efficient fund allocation, whether for equipment, expansion, working capital, or other essential needs. Additionally, a structured repayment strategy is crucial, demonstrating a clear plan to manage revenue, optimize cash flow, and ensure timely debt repayment.

- Loan Assessment and Financial Analysis: A thorough loan assessment and financial analysis can help determine the precise funding needed for your business. By evaluating expenses and potential fund utilization, you can gain a clearer understanding of your financial requirements. Ensuring that the loan amount aligns with your business needs can lead to more efficient borrowing and financial stability.

- Organizing Financial Documents: Keeping your balance sheets, income statements, and tax returns up to date can streamline financial processes and improve loan approvals. Having bank statements, financial reports, and any lender-specified paperwork readily available can help make applications smoother and more efficient.

- Establishing Business Credibility: Providing your business registration details, licenses, and certifications can strengthen your application. If applicable, including patents, trademarks, or proprietary formulas can further showcase your business’s uniqueness and credibility.

- Realistic Business Growth Projections: Clearly explaining how the loan will support your business expansion can strengthen your application. Using past performance data and market research to demonstrate growth potential and repayment capacity can provide lenders with valuable insights into your business’s future success.

7 Key Aspects to Be Mindful Of When Procuring Business Loans

The journey from loan preparation to procurement involves navigating several factors. What works for one business may not work for another, making it essential to understand the unique considerations that can impact the loan application.

It is necessary to assess multiple aspects to make an informed decision and improve the likelihood of the loan approval. The following key considerations should be considered:

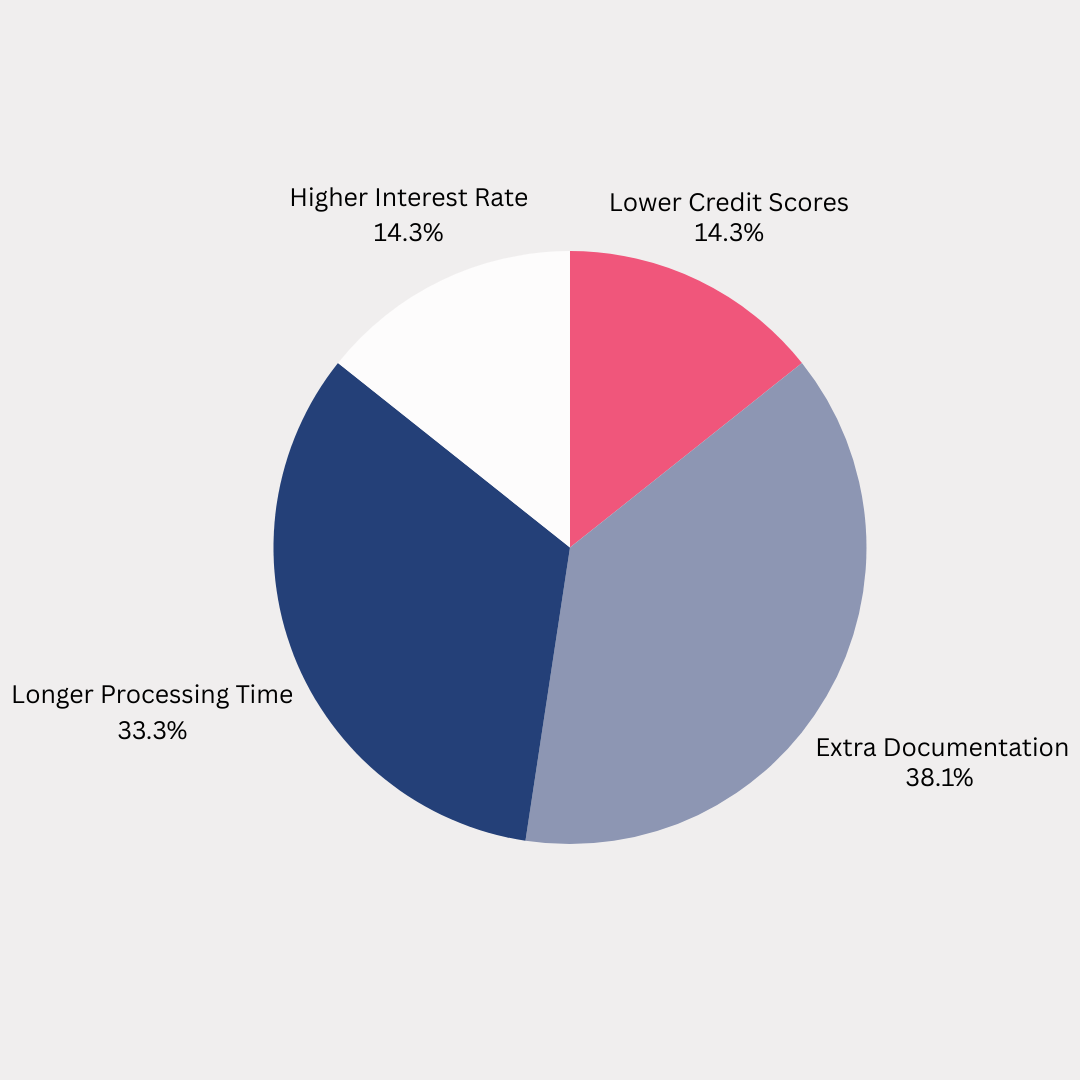

- Loan-to-Value (LTV) Considerations: Asset valuation affects loan amounts and interest rates. Women entrepreneurs often face slightly higher interest rates, averaging 1.5-2% more due to asset undervaluation. Accurate asset assessment can help secure better loan terms.

- Processing Time Expectations: Loan processing times vary. Women entrepreneurs applying for loans from traditional commercial banks may experience processing periods 35% longer compared to male counterparts. Prepare all documentation in advance and maintain clear communication with lenders.

- Documentation Requirements: Women entrepreneurs often encounter complex and tedious paperwork during the loan application process, leading to longer approval times and increased documentation requirements during the application process. Keeping financial statements, registration certificates, and other essential paperwork well-organized can help streamline the process and improve approval chances.

- Credit Score Considerations: A strong credit score is vital. CIBIL research shows that women-led MSMEs often receive credit scores 15-20 points lower than male counterparts despite similar business performance. This disparity stems from limited credit history, traditional asset ownership barriers, algorithmic bias against home-based businesses with shorter histories, among others. To improve creditworthiness, women entrepreneurs should monitor credit status, ensure timely payments, and manage debt responsibly. Financial institutions can help by implementing alternative scoring models using transaction histories and digital footprints, offering financial literacy programs, and creating gender-specific financial products to ensure more equitable credit access.

- Alternative Assessment Methods: Traditional collateral-based lending isn’t always the best fit. A World Bank study found that 68% of women-led MSMEs benefit from cash-flow-based lending, which evaluates business revenue instead of relying solely on physical assets.

Understanding Loan Terms Beyond Interest Rates:

- Repayments Schedule:

It is necessary to choose appropriate repayment schedules that align with business cash flow cycles. This ensures sustainable growth. According to the RBI UK Sinha Committee Reportenterprises using structured financial solutions tailored to operational cycles demonstrate 22% improved sustainability. For example, a seasonal business like a handicraft export company might benefit from a step-up loan structure with lower payments during slow seasons and higher payments during peak sales periods.

- Hidden Costs and Fees:

Often, the advertised interest rate does not clarify the total loan cost. Additional expenses, such as processing fees (typically 1-2% of the loan amount), prepayment penalties (which can range from 2-4% of the outstanding amount), and administrative charges for documentation and servicing, are not clearly mentioned. For instance, a ₹10 lakh loan with a 1.5% processing fee immediately reduces the received amount by ₹15,000, significantly affecting initial capital deployment.

- Collateral Requirements:

Women entrepreneurs frequently encounter challenges with traditional collateral requirements due to property ownership disparities and asset valuation issues. According to NITI Aayog data, only 14% of women in India own land, creating an inherent disadvantage in securing collateral-based loans. This gap has led to the development of alternative assessment methods, including cash flow-based lending, invoice financing, and inventory-backed loans that evaluate business performance rather than physical assets.

Navigating Loan Options:

Women entrepreneurs seeking business loans should be aware of the range of financing options available to them.

Usually, business loans from banks and NBFCs like Protium come with structured terms, collateral requirements, and detailed documentation. These include term loans for specific business investments, working capital loans for day-to-day operations, and lines of credit that allow businesses to draw funds as needed.

On the other hand, established businesses with existing loan relationships with financial institutions may find that seeking top-up business loans are slightly easy to get and have significant advantages such as:

- Fewer documentation requirements

- Faster processing times

- Potentially better interest rates due to established relationships

- Flexibility terms

Application Mistakes to Avoid

- Mixing Personal and Business Finances: A study by FICCI highlights 62% women entrepreneurs face loan rejection due to inadequate separation of personal and business finances. Lenders assess financial health based on business cash flow, profitability, and creditworthiness. Mixing finances makes it difficult to track business performance, leading to a lack of transparency. To avoid this, maintain separate bank accounts, keep organized records, and use accounting software to streamline financial management.

- Unrealistic Growth Projections: According to RBI data, 47% women-led MSME loan applications get rejected due to inconsistent or overly ambitious financial projections. Lenders rely on revenue forecasts, cash flow statements, and market trends to evaluate repayment capacity. Inflated projections without supporting data raise red flags. To improve approval chances, provide realistic growth estimates backed by past performance, industry benchmarks, and market research to demonstrate credibility and business stability.

- Avoiding Loan Term Negotiations: A SIDBI survey reveals that women entrepreneurs negotiate loan terms 30% less frequently than their male counterparts, often accepting the first offer without discussions. This can result in higher interest rates, shorter repayment periods, and restrictive terms. Negotiating can lead to better interest rates, flexible repayment options, and lower processing fees, reducing the overall cost of borrowing. Before signing any agreement, research available options, compare lenders, and confidently negotiate terms to secure a favorable deal.

Getting a business loan can help women entrepreneurs grow, but it’s important to plan wisely. Understanding loan terms, maintaining finances, and showing a clear growth plan can improve approval chances. Funding options offer great support but entrepreneurs must use them to build and expand with confidence. With the right approach, a loan can provide the financial support needed to grow and sustain a business.

Sources

1.Press Information Bureau December 2024 Report

2.SIDBI, SIDBI Report on MSME Finance (2022)

3.RBI Report on Trend and Progress of Banking in India (2020)

4.Bain & Co. & Google Powering the Economy with Her: Women Entrepreneurship in India” (2020)

5.CIBIL MSME Pulse – December 2023

6.World Bank Expanding Access to Finance for Women-Led Micro, Small, and Medium Enterprises (MSMEs): Evidence from Emerging Markets 2023

7.RBI UK Sinha Committee Report, Report of the Expert Committee on Micro, Small and Medium Enterprises, June 2019

8.NITI Aayog Data,2020

9.FICCI Study, FICCI Women Entrepreneurs, July 2012

10.RBI Data Report of the Expert Committee on Micro, Small and Medium Enterprises 2019

11.SIDBI Survey Impact Assessment of SIDBI’s Financial and Developmental Support to MSMEs 2022