Leverage Your Property’s Potential with Protium’s Loan Against Property

Solutions!

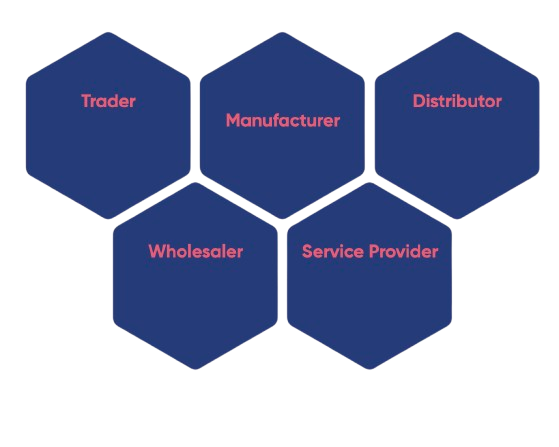

Protium’s Ideal Customer

Self-Employed Professionals/Business owners whose business has been

operational active for at least 3 years:

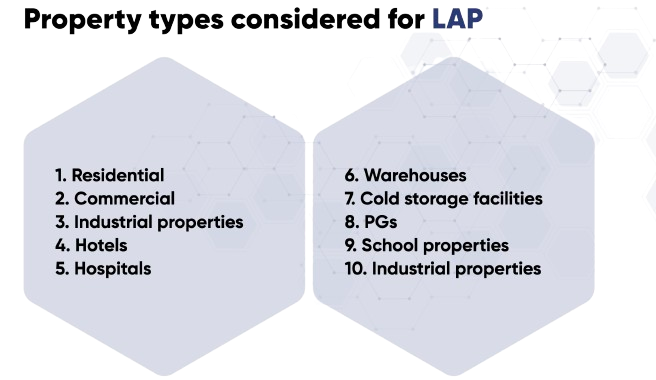

Image Display

Why Choose Protium?

Loan approval in 3-7 working days

Loan disbursal in 2-7 working days

Procure loan up to 80% of property value

No hidden charges

Minimal Documentation: Only the most important documentation that helps in assessing the loan application process is requested.

Interest Rate: Competitive rates that vary based on loan amount, tenure, and applicant profile.

Top-Up Loan: Existing customers can avail a top-up loan based on current criteria

Balance Transfer: Transfer loan amount for higher loan and attractive interest rates.

Disclaimer:

*Protium Finance Ltd (Protium) may use the services of various agents on its behalf for the purpose of sales and marketing for Protium’s products and services

*Terms and conditions apply, based on applicant eligibility and financial profile.