Policy on Co-Lending with Banks for Priority Sector

Version: 1.0

Introduction

Protium Finance Limited (“PFL”/ “the Company”) is a Systemically Important, Non-Deposit Taking, Non-Banking Financial Company (NBFC-ND-SI) focused on providing secured and unsecured lending to the MSME and consumer segment in India.

Preamble

RBI vide circular issued on November 5, 2020, having reference no. RBI/2020-21/63, FIDD.CO.Plan.BC.No.8/04/09/01/2020-21 (CLM Guidelines) have directed NBFCs to formulate board approved guidelines for entering into the arrangement with Bank(s) for lending to priority sector under Co-Lending Model (“CLM”).

The Board, pursuant to the above referred RBI circular, has formulated a policy which will be known as “Policy on Co-Lending with Banks for Priority Sector”

Eligibility

PFL can enter into CLM arrangements with all Scheduled Commercial Banks except SFBs, RRBs, UCBs, LABs & Foreign Banks (including WOS) having less than 20 Branches. (“Co-lender Banks”) Lending under CLM arrangements to be made only for priority sector as defined by RBI.

Master Agreement between PFL and Co-Lender Bank

A Master Agreement incorporating Terms and Conditions of CLM arrangement between PFL and Co Lender Bank shall be entered into which shall inter-alia include but not be limited to specific product lines and areas of operation, provisions related to segregation of responsibilities as well as customer interface and protection issues, necessary clauses on representations and warranties etc.

The Master Agreement shall provide for the model of CLM arrangement between PFL and Co-Lender Bank:

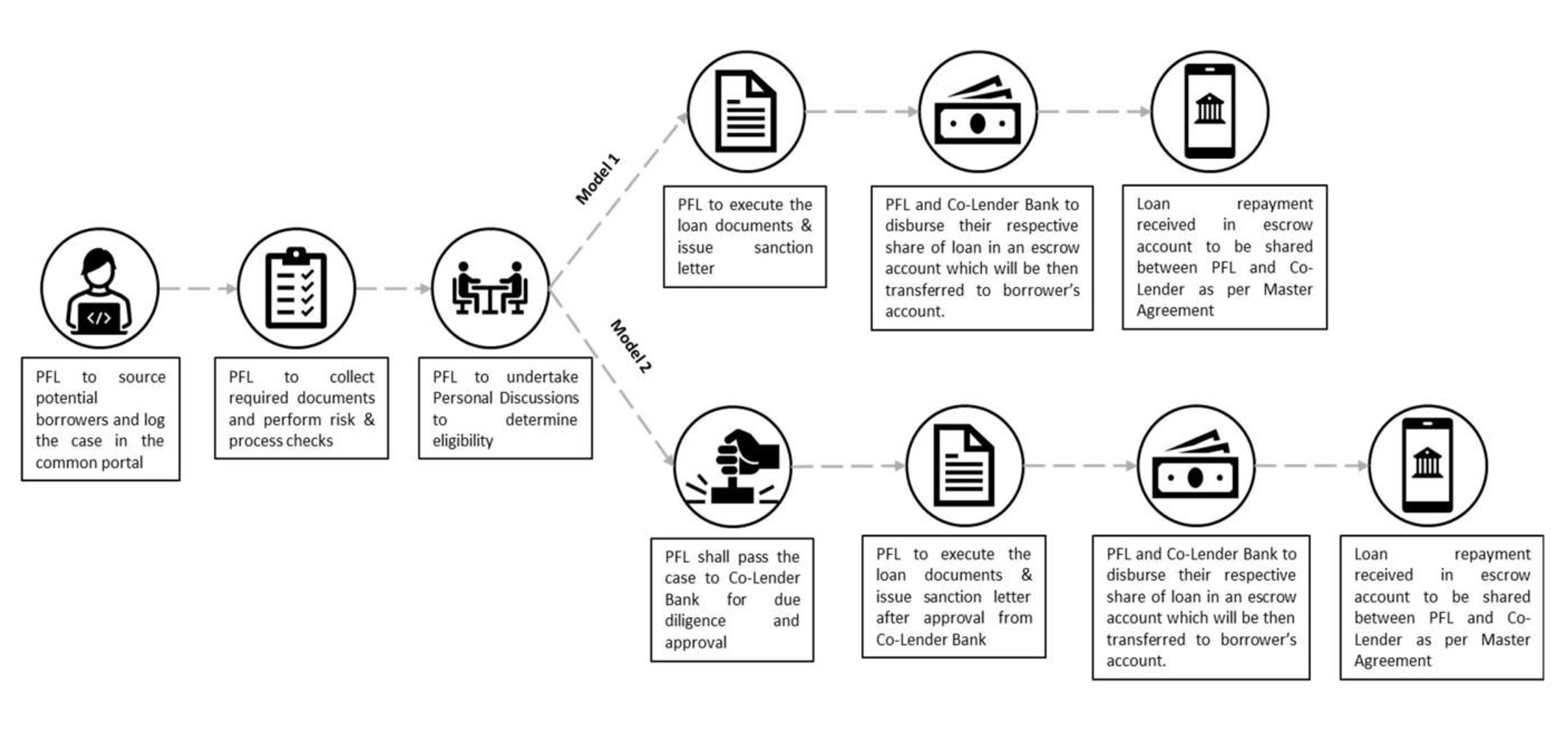

Model 1: Co-Lender Bank to mandatorily take their share of the individual loans, originated by PFL, in their books as per the terms of the Master Agreement

• If the Master Agreement entails a prior, irrevocable commitment on the part of the bank to take into its books its share of the individual loans as originated by PFL, the arrangement shall comply with the extant guidelines on Managing Risks and Code of Conduct in Outsourcing of Financial Services by Banks issued vide RBI Circular No. RBI/2014- 15/497/DBR.No.BP.BC.76/21.04.158/2014-15 dated March 11, 2015, updated from time to time.

• In particular, the Co-Lender Bank and PFL shall have to put in place suitable mechanisms for ex-ante due diligence by the bank as the credit sanction process cannot be outsourced under the extant guidelines on Outsourcing.

• The bank and PFL shall also comply with the Master Directions – Know Your Customer (KYC) Direction, 2016, issued vide RBI/DBR/2015-16/18 Master Direction DBR.AML.BC.

No.81/14.01.001/2015-16 dated February 25, 2016 and updated from time to time, which permit regulated entities, at their option, to rely on customer due diligence done by a third party, subject to specified conditions.

Model 2: Co-Lender Bank to retain the discretion to reject certain loans after their due diligence prior to taking in their books.

• Where the Co-Lender Bank exercise its discretion regarding taking into its books the loans originated by PFL as per the Master Agreement, the arrangement will be akin to a direct assignment transaction.

• Accordingly, the Co-Lender Bank shall ensure compliance with all the requirements in terms of Guidelines on Transactions Involving Transfer of Assets through Direct Assignment of Cash Flows and the Underlying Securities issued vide RBI/DOR/2021-22/86 DOR.STR.REC.51/21.04.048/2021-22 Master Direction – Reserve Bank of India (Transfer of Loan Exposures) Directions, 2021, as updated from time to time, with the exception of Minimum Holding Period (MHP) which shall not be applicable in such transactions undertaken in terms of this CLM.

• The MHP exemption shall be available only in cases where the prior agreement between the banks and PFL contains a back-to-back basis clause and complies with all other conditions stipulated in the guidelines for direct assignment.

Sharing of Risks and Rewards

PFL will accept minimum 20% share of individual loan in its book till maturity and the CoLender Bank will take the balance share of the individual loans on a back-to-back basis in their books. The actual % share of individual loans in all cases shall be guided by the terms of Master Agreement.

Co-Lending Product

Detailed credit products, processes, programs etc. will be finalized and documented in the Master Agreement with the Co-Lender, on case-to-case basis, keeping in view the target segment, area of operations, other operational issues, recovering mechanism etc.

Credit Norms

PFL and Co-Lender Bank shall mutually agree upon the various parameters and norms for assessment of credit applications based on the extant applicable RBI guidelines and respective internal policies.

Interest Rate & Other Charges

Subject to credit policy of PFL, as updated/amended from time to time, PFL shall offer its rate of interest on Fixed rate / Floating rate basis in accordance with the extant guidelines applicable to it. The Co-Lending Bank shall charge rate of interest for their part of exposure in accordance with the extant guidelines applicable to it and their internal pricing policies, however, the ultimate borrower shall be charged an all-inclusive blended interest rate.

Upon repayment, the interest shall be shared between PFL and the Co-Lender Bank in proportion to their share of credit and interest.

Any other applicable charges shall be decided mutually between PFL and Co-Lender Bank and shall be communicated to the borrower.

Fees may be payable to PFL for sourcing, collection, servicing, or any other purpose. This amount will be negotiated with Co-Lender Bank and shall be documented in the Master Agreement.

Escrow Account

All transactions (disbursements/ repayments) between the Co-Lender Bank and PFL relating to CLM arrangement shall be routed through an escrow account maintained with banks, in order to avoid inter-mingling of funds. The Master Agreement shall specify the manner of appropriation between PFL and Co-Lending Bank.

Security & Charge Creation

PFL along with Co-Lending Bank shall arrange for creation of security and charge as per mutually agreed terms.

Monitoring & Recovery

There shall be a system and framework for monitoring of all the process viz. Loan Origination, Loan Management, Disbursements, Collection and Recovery in consultation with respective Co-Lending Bank.

The loans under the CLM shall be included in the scope of internal/statutory audit to ensure adherence to our internal guidelines, terms of the agreement and extant regulatory requirements.

Provisioning and Reporting Requirement

PFL shall adhere to the asset classification & provisioning requirement including as per the respective regulatory guidelines, from time to time and also report to Credit Information Companies, under applicable law & regulations for its portion of lending.

Assignment

Any assignment of Co-Lender Bank’s share of loan shall be done only with the consent of PFL and vice-versa.

Customer Related Issues

PFL shall be the single point of interface for the borrowers and shall enter into a loan agreement with the borrower, which will clearly contain the features of the CLM arrangement and roles and responsibilities of PFL and Co-Lender Bank.

All the details of arrangement shall be disclosed to the borrower upfront and explicit consent of the borrower shall be taken on the same.

The extant guidelines relating to customer service and fair practices code and the obligations enjoined upon the Banks and PFL therein shall be applicable mutatis mutandis in respect of loans given under the CLM arrangement.

PFL shall generate a single unified statement of the borrower, through appropriate information sharing arrangements with the Co-Lender Bank

Grievance Redressal

Suitable framework shall be put in place upon mutual consideration, to share and resolve any complaint registered by a borrower with the PFL/ Co-Lender Bank within 30 days, failing which the borrower would have the option to escalate the same with the concerned Banking Ombudsman/Ombudsman for NBFCs or the Customer Education and Protection Cell (CEPC) in RBI.

Dispute Resolution

Dispute Resolution framework shall be part of the Master Agreement between PFL and Co-lender. PFL shall ensure inclusion of clauses relating to manner of dispute resolution as agreed with the Co-Lender.

Business Continuity Plan

A business continuity plan shall be formulated upon mutually agreed terms, to ensure uninterrupted service to the borrowers till repayment of the loans under the CLM agreement, in the event of termination of CLM arrangement.

Validity Period of Policy

The Policy shall be valid up to 5 years from the date of approval however, the Policy shall be subject to periodic review at least annually in accordance with any regulatory or statutory requirement and shall be approved by the Board.

Board will be informed periodically for overall limits of co-lending as a percentage of AUM.

Process Flow of Co-Lending Arrangement in Brief

Note: The above process is Business as Usual. The detailed and specific process shall vary case-to-case basis and shall be incorporated in the Master Agreement.