How can the Protium app transform the SME lending landscape?

Synopsis: In today’s blog, we will examine the trends and dynamics of the SME lending landscape and the pivotal role played by Protium in transforming this credit ecosystem.

In India, the small and medium enterprises (SME) sector, including micro-enterprises has been a critical driver of job creation, social cohesion, growth, and innovation. With over 63.4 million enterprises employing almost 111 million people, the MSME sector has contributed over 30% to India’s GDP.

But SMEs continue to be plagued by the long-standing hurdle of accessing affordable finance, which is vital for starting, sustaining, and growing their businesses. As per the UK Sinha Committee report, the credit gap in the MSME segment stands at Rs. 20-25 lakh crore.

With less than 15% of SME lending coming from formal sources, there is ample opportunity to digitalize the credit underwriting processes and for new business models to emerge that can bridge this critical credit gap—and Protium has been doing exactly that.

So, what is the current SME lending scenario like, and how can this landscape be revolutionized to future-proof our SMEs and the economy?

SME Lending Market: An Outline

As per some estimates, the Indian MSME sector has a whopping Rs. 69.3 trillion credit demand, which is currently growing at an 11.5% CAGR. While loan disbursements have improved—a fact corroborated by the latest SIDBI MSME Pulse report—far more needs to be done.

The Q2 FY23 Pulse report states that loan disbursements to the MSME sector have grown 24% year-on-year, with the micro sector accounting for the highest growth at 54%, followed by the small and medium enterprises sector at 23% and 9%, respectively. Indeed, micro-enterprises, which constitute 97% of the MSME segment, now account for 25% of its loan portfolio.

A major chunk of this growth can be attributed to the growing formalization of MSMEs and their embrace of digital and platform-based services. Today, almost 72% of payments are made digitally to MSMEs, which provides lenders with additional data, making credit underwriting and loan processing easier.

In fact, the availability of alternate data sources and the targeting of consumers in Tier III and beyond cities by new-age lenders have resulted in the sanction of over 50% of the new MSME loans to new-to-credit (NTC) borrowers.

But what is fueling this MSME loan growth, and how is Protium contributing to this credit revolution? Let’s find out.

SME Lending Market: Trends and Opportunities

According to India’s CEA, MSME lending is due to reach Rs. 3 trillion by FY23, supported by several government initiatives, including the Account Aggregator (AA) framework, TReDS, AEPS, Mudra, India Stack, and the Open Credit Enablement Network (OCEN). Besides, with lenders adopting cutting-edge technologies and opting for cash-flow-based lending models, borrowers can access tailored, sachet-sized loans through end-to-end automated processes.

1. Digitalization and Automation

Automated systems, artificial intelligence (AI), machine learning (ML), and blockchain technology have transformed SME lending by systematizing the entire lending value chain, from application processing, screening, and creditworthiness assessment to final collection.

By reducing application-to-disbursal times and deploying self-correcting AI/ML models, lenders are assured of higher credit offtake with lower default risk. To illustrate, Protium has designed its own engineering-led proprietary technology that ascertains borrowers’ creditworthiness based on their revenue and growth data.

2. API Integration

With consent-led architecture in place with the launch of the AA framework, it has become easier to integrate Application Program Interfaces (APIs) in digital lending products, creating scope for quick loan sanctions and personalization. Moreover, these APIs can be connected to third-party vendors when suitable for automating workflows, reducing errors, and improving overall efficiency.

3. Embedded Finance

Embedded finance allows for the integration of financial services on a non-financial platform and has become fairly popular for its lending purposes. Lending products like Buy Now, Pay Later (BNPL) loans are increasingly being utilized by online shoppers to meet their short-term, immediate needs.

Now that we know the factors that are reshaping the lending industry, let’s understand what really goes into designing an SME lending model and how Protium does it even better.

SME Lending Model: Building Blocks

Generally, a lending model comprises four major blocks: strategy, processes, analytics, and the final model design.

1. Define a Strategy

Owing to the diversity of SME enterprises, lenders design their strategies after accounting for factors such as target segments, pain points, distribution channels, product offerings, and value propositions. For instance, Protium follows a blend of physical and digital processes, allowing its borrower segment the bandwidth to move in and out of the tech stack as per its requirements.

2. Design the Process

One of the biggest deterrents to SME lending is the delay in loan processing. Thus, after determining their strategy, lenders streamline their processes in such a way that most of the customers experience straight-through processing to cut down on turn-around times, with only the unique cases going through manual checks.

3. Conduct Analytics

With SMEs leaving a digital footprint, lenders can now access alternate sources of data and glean operational insights into sales, payments, and social media metrics through their predictive models. So, by conducting analytics, they improve their decision-making by keying real-time data into their models and further leveraging it to cross-sell other financial products.

4. Optimize the Model

As SMEs require bespoke loan products, digital lenders must provide differentiated customer journeys. However, this extensive level of customization can complicate the model, creating scope for software entropy. Thus, lenders tend to create flexible models that can easily accommodate such variations to avoid system breaches and slow processing — with Protium leading this through a pre-eminent engineering-led lending model.

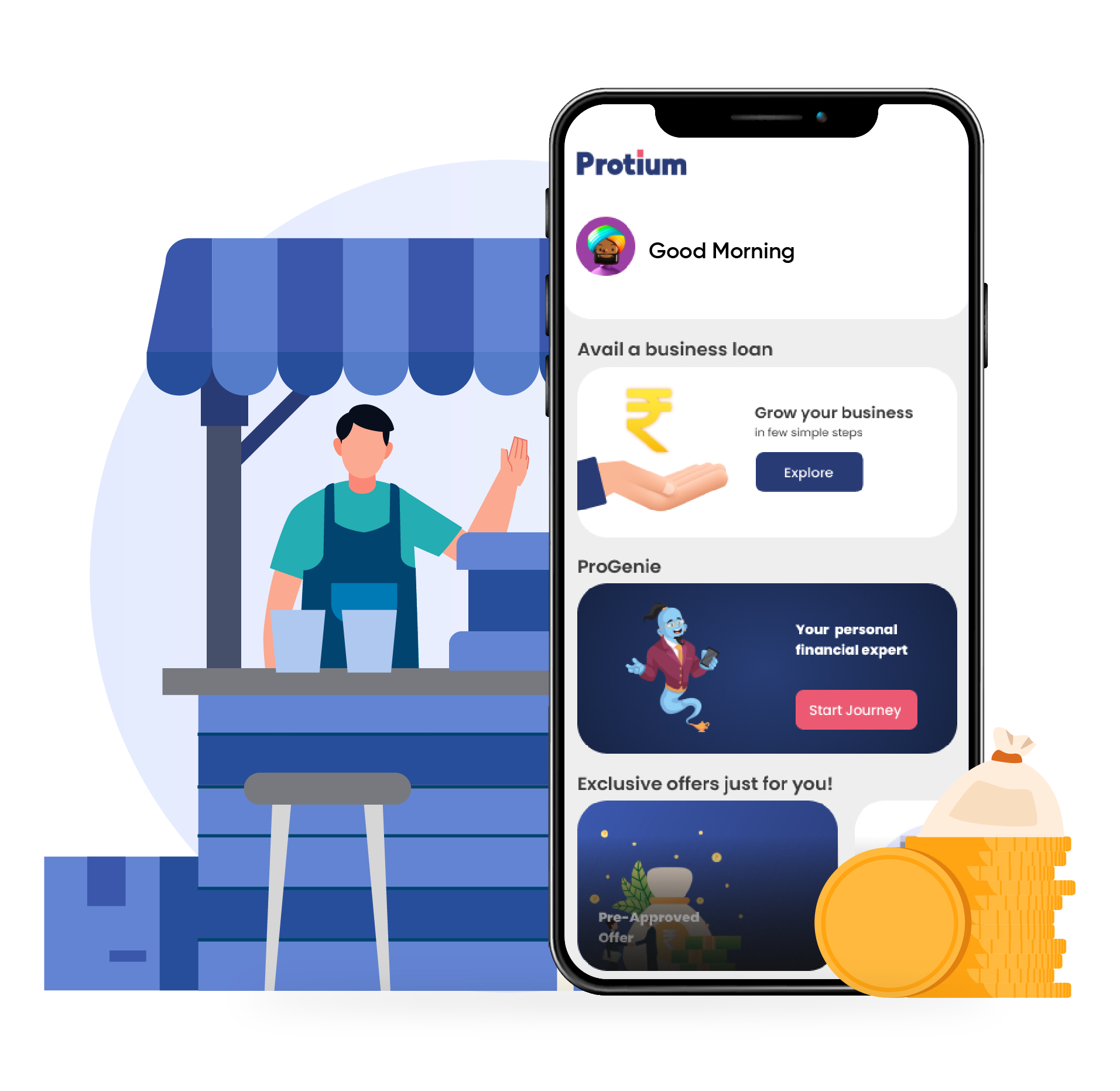

But how does the Protium app revolutionize the SME lending ecosystem?

Protium App: The True Game Changer for SME Lending

With over 25 million transactions processed and disbursements exceeding INR 5,300 crore, Protium has been trailblazing massive growth in SME lending across multiple segments through its offline and online business models. And now with the advent of the Protium app, the current lending landscape is poised for a major transformation.

1. Quick Processing

Protium’s proprietary models are adept at digitally collecting and processing all customer data in record time and extending loans in the shortest time. In some cases, business loan funds are disbursed in as little as three days from the app.

2. Superior Creditworthiness Evaluation

Your lack of credit history is no longer the end-all criterion when applying for a business loan. The Protium app has been optimized to consider several additional factors, including your cash flows, bank statements, and transaction data, for determining your creditworthiness, making it easier to apply for loans.

3. Hyper-customization

On the Protium app, you can avail of personalized loans that are tailored to your requirements, ranging from small, sachet-sized personal loans to business loans and equipment finance requiring considerable sums with flexible repayment schedules.

4. Omnichannel experience

In a lending ecosystem fixated on creating digital-only processes, Protium sets itself apart by enabling potential borrowers to initiate their loan journey from the app while leveraging the services of our agents present at the physical branches.

Conclusion

In a nutshell, the Protium App offers a wide variety of loan products, including SME finance, LAP, machinery finance, consumer credit, and more, that are tailored to business requirements. You can additionally check your credit scores for free on the app while availing of personalized loan offers most suited to your needs. Download the Protium app now and fuel the growth of your business.