Schemes and Union Budget 2026-27 Announcements Women-Led MSMEs Must Know

- This Women’s Day, we shed light on women-led MSMEs, which form a significant part of India’s registered enterprise base, and on how their share in investment and turnover can be strengthened.

- Recent policy efforts focus on three clear areas—simpler registration, improved credit access through guarantees and subsidies, and stronger market linkage through procurement and retail platforms.

- Initiatives such as SHE-Marts and the SME Growth Fund were introduced in the Union Budget 2026-27 to improve organised selling channels and scale-ready enterprises.

- The real measure of success will be more women-led MSMEs with steady sales records, stronger lender confidence, and sustainable participation in organised markets, including those in Tier-2 and Tier-3 regions.

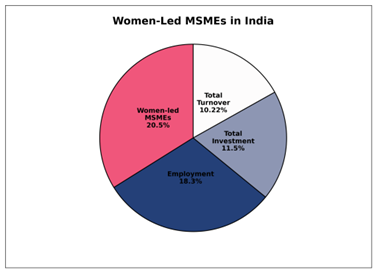

Women-owned businesses account for 20.5% of the total registered MSMEs in India. Their enterprises contribute 18.73% to employment generated, 11.15% to total investment, and 10.22% to total turnover among registered MSMEs1. The outreach spans urban centres as well as Tier-2 and Tier-3 towns, where home-led production units, family-run retail shops, small manufacturing setups, beauty and service microbusinesses form the backbone of local economies.

These markets carry a higher share of informal activity and depend heavily on local credit networks and community-based selling. In fact, women-owned Informal Micro Enterprises (IMEs) account for 70.49% of total registrations and 70.84% of employment in this category. While it’s apparent that women are already active in enterprise, policy is also focused on helping them formalise and scale.

This Women’s Day, here’s a look at how government initiatives are increasingly focused on practical business support for women-led MSMEs through easier credit access, skill development, and stronger market opportunities.

Three Areas Women-Led MSMEs Must Implement

1. Formal registration

Special drives have been introduced to encourage more women-owned enterprises to register on the Udyam portal. Formal registration helps businesses access credit, participate in government procurement, and build credibility with lenders and buyers.

2. Improved access to credit

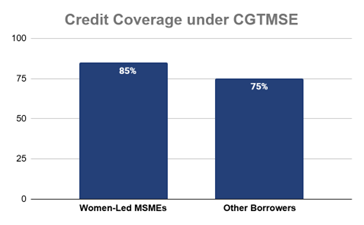

Formal registration leads to easy access to finance through targeted concessions and guarantee enhancements. For example, under the Credit Guarantee Scheme for Micro and Small Enterprises, women entrepreneurs receive a 10% concession in annual guarantee fees and higher guarantee coverage of up to 85%, compared to 75% for other borrowers.

3. Market access and business exposure

Government procurement rules and marketing initiatives have created more opportunities for women-led MSMEs to reach institutional buyers and participate in trade fairs and exhibitions. Several initiatives already support these priorities across credit access, capability development, and market linkage. These include:

- The Prime Minister’s Employment Generation Programme (PMEGP) was launched in 2008 and provides higher subsidy support to women, helping them establish microenterprises.

- Public procurement norms were amended in 2018 to require Central Ministries, Departments, and Public Sector Undertakings to procure at least 3% of their annual purchases from women-owned micro and small enterprises.

- The Procurement and Marketing Support Scheme guidelines were revised with effect from November 2019, providing higher subsidies to support women-owned MSMEs in participating in trade fairs and reaching buyers beyond local markets.

- The “SAMARTH” initiative was launched in March 2022, reserving 20% seats in free skill development programs, 20% participation in MSME business delegations for exhibitions, and a 20% discount on annual processing fees under NSIC schemes, with a target to train over 7,500 women from rural and sub-urban areas.

- The MSME Sustainable ZED Certification Scheme was launched in April 2022 and includes a provision of 100% subsidy on the cost of ZED certification for women-owned MSMEs.

- Under the Credit Guarantee Scheme for Micro and Small Enterprises, provisions effective from December 2022 provide women entrepreneurs a 10% concession in annual guarantee fees and additional guarantee coverage up to 85%, compared to 75% for others.

- The Lakhpati Didi Program, launched in 2024by the Ministry of Rural Development, aims to empower women in Self-Help Groups (SHGs) to earn a sustainable annual income of ₹1 lakh or more per household. It focuses on enabling sustainable livelihoods, fostering entrepreneurship, and boosting rural economies

Aditionally, the recent Union Budget 2026–27 takes the same direction a step further by adding a clearer pathway for sales and visibility through structured retail channels. Here are some key announcements that push women-led enterprises by combining online marketplaces, enterprise transition support, and broader MSME growth measures:

- SHE-Marts: A new initiative to set up community-owned retail outlets within cluster-level federations, built to improve market access for women-led enterprises and help them sell in a more organised way.

- SME Growth Fund: A ₹10,000 crore SME Growth Fund aimed at supporting the emergence of “champion SMEs.” Women-led enterprises that demonstrate scalable business models and strong market demand can benefit from such growth-focused financing and investment support.

- Infrastructure Support: The Budget proposed one girls’ hostel in every district through VGF/capital support, strengthening access for women in higher education, especially in technical/STEM pathways.

- Reinforcing SHG-to-Enterprise Pipeline: The Union Budget also continues support for the Deendayal Antyodaya Yojana – National Rural Livelihoods Mission (DAY-NRLM), a flagship programme that promotes women’s Self-Help Groups across rural India. The mission helps women build savings discipline, access credit, and start income-generating activities through SHG networks.

The National Scheme Stack for Women Entrepreneurs

Government support for women entrepreneurs spans credit, subsidy, training, and market development. The key is not to approach all schemes simultaneously, but to understand where each fits in the business lifecycle.

- MUDRA: The Most Common Starting Point

MUDRA loans serve as a practical entry point for collateral-free credit. Small-ticket funding under Shishu, Kishor, and Tarun categories aligns with micro-enterprises at different growth stages. For many women-led units, such loans support inventory purchase, raw materials, small machinery, or working capital smoothing.Aligning loan size with turnover, maintaining clear bank records, and ensuring repayment comfort strengthen long-term credit access.

- Stand-Up India

Stand-Up India caters to women planning larger ventures in manufacturing, trading, or services. Loan sizes are higher and suited to structured unit setups or capacity expansion.

- TREAD

The Trade Related Entrepreneurship Assistance and Development (TREAD) scheme recognises that funding alone does not address pricing errors, costing gaps, or marketing challenges. It integrates training, counselling, and credit linkage through implementing agencies.

This model suits first-generation entrepreneurs and women-led micro units that require guided handholding before approaching formal lenders independently.

- Other Women-Centric Schemes MSMEs

Several additional schemes are frequently discussed in business circles. Their effectiveness depends on carefully matching them to the business type and stage:

- Udyogini: Udyogini supports small and local enterprises, often with concessional terms. It is relevant to petty trade, service units, and micro-production activities.

- Mahila Udyam Nidhi (SIDBI): Mahila Udyam Nidhi supports women-led units seeking small-scale expansion. Funding may be directed toward machinery purchase, capacity enhancement, or operational strengthening. The scheme aligns with enterprises that have stabilised operations and are ready for incremental growth.

- Sector-linked schemes such as the Mahila Coir Yojana: Sector-specific schemes, such as the Mahila Coir Yojana, provide training and equipment support tailored to traditional or cluster-based industries. When women-led enterprises operate within a defined skill ecosystem, such focused support reduces experimentation and improves production efficiency.

Things to Consider Before opting for the right govt scheme

Women business owners could consider the following before choosing the right kind of support:

- Match the scheme to the Business Stage

Early-stage units may prioritise entry-level credit or training-linked programs. Stabilising enterprises may seek working capital support. Scaling businesses may consider expansion-focused loans or market-access schemes.

- Identity and Registration Basics

Clear identity documents, Udyam registration (where applicable), clean banking transactions, and basic sales records build lender confidence and simplify approvals.

- Credit Use That Supports Daily Operations

Credit aligned to actual business needs protects margins. Maintaining a repayment buffer improves long-term stability and cashflows.

Strengthening women-led MSMEs should translate into measurable business progress. More enterprises with stable monthly sales records and stronger lender confidence would indicate meaningful improvement. More micro units moving from one-time borrowing to repeatable growth and organized market participation would reflect real enterprise building. Clearer last-mile delivery, particularly in Tier-2 and Tier-3 regions through district facilitation, state-level programs, and structured selling platforms like SHE-Marts, would demonstrate that policy intent has reached business reality.