7 Udyam Registration Benefits that are Strengthening 7.94 crore Indian MSMEs

Udyam has moved beyond a simple certificate to become a critical growth tool for India’s MSMEs. It serves as a gateway for small businesses in Tier-2 and Tier-3 cities to transition from informal operations to a recognised, credit-ready status. This blog article lists 7 such advantages, ranging from formal credibility and government procurement access to delayed payment protection and digital system preparedness.

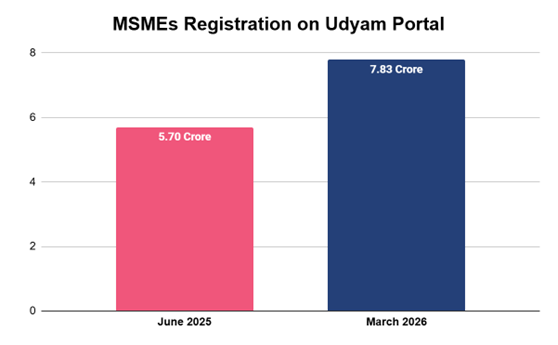

India’s Udyam registration ecosystem has become one of the strongest signs of MSME formalisation. By June 26, 2025, more than 5.70 crore MSMEs were registered on the Udyam Registration and Udyam Assist platforms. More recent official data on the Udyam portal shows that this number crossed 7.94 crore enterprises by April 2026, reflecting the speed at which small businesses are entering the formal ecosystem.

This growth shows that MSMEs are not registering only for a certificate. They are registering because Udyam is becoming a gateway to finance, government schemes, delayed payment protection, procurement opportunities, and better business credibility. For small manufacturers, traders, workshop owners, service providers, and local enterprises in Tier-2 and Tier-3 cities, Udyam registration is now becoming a practical business tool.

Here are 7 ways in which MSMEs are benefiting from registration.

1. Formal Business Identity & Credibility

For many MSMEs, the first real benefit of Udyam registration is formal recognition. A small business may have operated for years with loyal customers, regular suppliers, and steady demand. However, without a formal identity, it may still find it difficult to approach lenders, apply for schemes, or participate in larger business opportunities.

Udyam registration helps small businesses move from informal operations to recognised business status. The registration process is online, paperless, and free, making it easier for smaller businesses to complete it without extensive compliance support. A registered business often appears more credible than an informal unit with no official enterprise identity. This can help when dealing with lenders, large buyers, suppliers, distributors, digital platforms, and business partners.

2. Access to MSME Loans, NBFC Support and Priority Sector Lending

A business may need funds to buy raw materials, maintain inventory, upgrade machinery, manage seasonal demand, or complete a large order. Udyam registration helps lenders identify the enterprise as an MSME. This matters because MSME lending is connected to India’s Priority Sector Lending framework. When a business has a valid MSME identity, lenders can assess it within a more defined category instead of treating it as an entirely informal borrower.

RBI-regulated NBFCs like Protium can support MSMEs with financing options linked to business needs, such as working capital, machinery finance, business expansion finance, and Loan Against Property. MSMEs can use such credit for several business purposes, including buying or upgrading machinery, expanding production capacity, managing seasonal working capital needs, taking larger orders, opening a new branch, outlet, or workshop, strengthening inventory before peak demand, and investing in storage, equipment, or business infrastructure.

Informal Micro Enterprises with Udyam Assist Certificates are treated at par with Udyam-registered enterprises for Priority Sector Lending benefits. This is especially important for microenterprises that may not have a long banking history, substantial collateral, or detailed, audited records.

3. Access to Government Schemes and Subsidies

Udyam registration also helps MSMEs access schemes offered by the Ministry of MSME and other government departments. These may include credit-linked schemes, technology upgrade support, cluster development support, market development assistance, skill development programs, and capacity-building initiatives.

Many schemes require a valid Udyam registration number before an MSME can apply. This reduces confusion for small business owners because Udyam acts as a common starting document for multiple benefits. Instead of treating every scheme as a separate entry point, MSMEs can use Udyam registration as their base identity.

4. Integration of Informal Micro Enterprises (Udyam Assist)

Many micro businesses do not have GST registration but still need formal recognition. SIDBI states that the principal objective of the MSME Formalisation Project is to provide Udyam registration to informal micro enterprises not registered with GST authorities. Udyam Assist has been developed with regulated entities, such as banks, NBFCs, MFIs, and government departments, acting as Designated Agencies to help informal microenterprises register.

Udyam Assist gives them a way to become visible in the formal economy. This visibility can support future access to credit, government support, and institutional opportunities.

5. A Route to Address Delayed Payments

Delayed payments are a serious challenge for MSMEs. A small enterprise may supply goods on time but receive payment weeks or months later. This affects working capital, salaries, supplier payments, raw material purchases, loan EMI payments, and order execution.

Udyam registration gives eligible micro and small enterprises access to the MSME Samadhaan delayed payment monitoring system. The portal allows micro and small enterprises with a valid Udyam registration to apply for delayed payment cases. (samadhaan.msme.gov.in) This benefit is especially useful for businesses supplying to larger buyers, corporates, government departments, or institutional customers.

6. Access to Government Procurement

Udyam registration can help MSMEs participate more confidently in government procurement. Many tenders, public procurement benefits, and buyer platforms require MSME recognition. Registered MSMEs can also explore opportunities through platforms such as GeM, depending on eligibility and product category. This can help local manufacturers, traders, fabricators, equipment suppliers, packaging units, food processors, and service providers expand beyond limited local buyer networks.

7. Preparedness for Digital Business Systems

Digital growth requires business identity, documentation, payment records, digital onboarding, and credit readiness. Udyam registration helps MSMEs become more prepared for this shift. Registered businesses can more easily explore digital lending, government portals, procurement platforms, formal payment systems, e-commerce channels, ONDC, and marketplace onboarding.

However, the value of Udyam registration depends on how actively MSMEs use it after registration. A certificate by itself may create formal identity, but the real benefit comes when the business connects it with finance, schemes, procurement, records, and digital systems. This is where a practical approach becomes important.

Practical Checklist: How MSMEs Can Use Udyam Registration Better

MSMEs can strengthen the value of registration by following a few practical steps:

- Keep Business Details Updated: MSMEs should ensure that the Udyam certificate reflects the correct business name, activity, address, and other key details.

- Align Business Records: Bank statements, GST filings, income documents, and other records should match the business information used during registration.

- Use Udyam for Loan Applications: MSMEs should include Udyam registration details while applying for loans from banks or RBI-regulated NBFCs.

- Track Government Scheme Eligibility: Businesses should regularly check relevant government schemes, subsidies, and support programs linked to MSME registration.

- Register on Buyer Platforms: MSMEs supplying goods or services should explore buyer, procurement, and marketplace platforms where formal registration is useful.

- Use Delayed Payment Support: When payments are stuck, eligible MSMEs can use MSME Samadhaan or other relevant delayed payment routes.

- Maintain Proper Transaction Records: Clean invoices, purchase orders, delivery records, and payment proofs strengthen credibility and creditworthiness.

- Borrow Based on Business Needs: MSMEs should plan borrowing around actual requirements, such as machinery, working capital, inventory, or expansion.

- Maintain Repayment Discipline: Timely repayments help businesses build a stronger credit profile for future financing needs.

- Treat Udyam as a Growth Tool: Udyam registration should be used as part of a larger formalisation journey, not just as a one-time certificate.