MSME Credit at ₹46 Trillion: How Small Businesses Can Borrow Smartly in 2026

- Even as MSME credit continues to grow, small businesses need stronger planning before taking new loans. Smart borrowing means using credit with a clear business purpose such as working capital requirements, machinery, stock purchase, order execution, or planned expansion.

- Expansion should be based on cash flow, not just demand. MSMEs should check upfront costs, payment timelines, working capital gaps, and repayment comfort before accepting larger orders.

- While credit can help MSMEs grow and reduce risk, formal borrowing can support diversification, improve records, build repayment history, and help businesses avoid over-dependence on one buyer, supplier, or market.

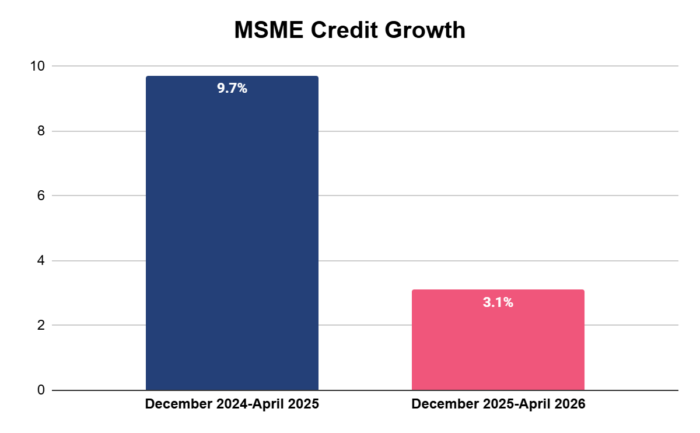

MSME loans stood at around ₹46 trillion in April 2026, growing 12.8% year-on-year. However, credit growth between December 2025 and April 2026 slowed to 3.1%, compared with 9.7% in the same period last year. Active MSME loans also declined by 3.5%, showing a more cautious lending and borrowing environment.¹ These numbers show that credit is still flowing to MSMEs, but lenders and borrowers are becoming more cautious. For small businesses, this matters. Expansion is still possible in 2026, but it needs better planning.

Global trade tensions, geopolitical risks, rising input costs, and supply chain pressures are making business planning more complicated. That is why smart borrowing in 2026 is not about taking on more loans. It is about borrowing with purpose, repayment discipline, and risk protection.

How 2026 is a Different Borrowing Year for MSMEs

MSMEs are facing a mixed business environment in 2026. There are growth opportunities, but there is also more uncertainty. Many small businesses may see demand from new markets, new customers, government-led infrastructure growth, digital commerce, and sector-specific expansion. At the same time, global issues are affecting local business conditions.

Trade disruption can affect raw material costs, export demand, shipping timelines, and supplier reliability. Even a business that serves local customers may depend on stock, parts, tools, or materials coming from another city, state, or country.

From the lenders’ perspective, credit is still available, but applications are being checked more carefully. Lenders may look closely at cash flow, repayment history, business stability, and documents. MSMEs also need to be careful. A loan taken without a repayment plan can create pressure later.

So, 2026 is not a year to avoid expansion. It is a year to expand with better cash-flow planning.

Planning Expansion Around Cash Flow, Not Just Demand

A large order may look like a clear growth opportunity, but it does not always bring immediate profit. In many small businesses, expenses come first and payments come later.

New orders may require spending on raw material, labor, packaging, transport, inventory, and overtime wages. If the buyer is a larger company, payment may come after 30, 60, or 90 days. Meanwhile, suppliers, workers, rent, electricity bills, fuel costs, machine maintenance, and vendor payments still have to be managed on time.

That is why MSMEs should look beyond the order value. They should check the cash flow needed to complete the order.

The same applies to traders and service businesses. A trader may stock up before seasonal demand, but if sales slow down or payments get delayed, money gets blocked in inventory. A service MSME may hire staff for a new client, but payment may start only after project delivery.

MSMEs should calculate the working capital gap before accepting larger orders. This means checking how much money is needed upfront, how long the money will remain blocked, and whether existing cash can support regular business expenses during that period.

Expansion should be supported by planned credit, not last-minute borrowing. Planned borrowing gives MSMEs more control over cost, repayment, and business decisions.

The New Role of Credit: Growth and Protection

For many years, MSME credit has been seen mainly as a growth tool. A business takes a loan to buy machinery, open a new shop, increase stock, hire people, or serve more customers. While that remains relevant, credit has another role in 2026. It can also help protect the business.

Delayed payments, raw material price changes, logistics disruption, and seasonal slowdown can create urgent funding needs. These are not always expansion costs. Sometimes, they are stability costs.

Credit can also help MSMEs avoid a bigger risk: dependency. Many small businesses depend on one large buyer, one main supplier, one product line, or one local market. This may work during stable times. But when uncertainty rises, dependency becomes risky. If one buyer delays payment or one supplier increases rates, the business may face pressure.

The right loan can protect daily operations while supporting long-term growth. It can help MSMEs keep enough liquidity, invest in useful upgrades, and reduce pressure during difficult months. But this works only when the loan has a clear purpose and repayment plan.

Credit should not become a patch for poor planning. It should become part of better planning.

Borrowing for Diversification

Expansion is not only about adding more stock, machines, workers, or orders. In 2026, MSMEs should also check whether expansion can reduce business risk. Using credit to diversify can be smarter than using credit only to increase capacity.

Workshops can add machinery to serve a new customer segment

A unit that serves only one automobile component buyer may use finance to add a machine that also helps it serve electrical, fabrication, or repair-related customers. This does not mean changing the entire business. It means creating one more revenue path.

For example, Comtech Industries used Protium’s Machinery & Equipment Loan to move beyond dependence on one major automobile buyer and enter the Power Sector with refurbished Power Press Machines. With Protium’s support, the business procured 5 machines instead of 1, targeting a 43% turnover increase and a 25% reduction in single-client dependency.

Traders can add faster-moving inventory categories

If one product category has become slow or price-sensitive, a trader can use planned working capital to add products with more regular demand. This helps improve cash rotation.

Manufacturers can build capacity for multiple buyers or sectors

This is especially useful when one industry becomes slow. If the business can serve two or three sectors with the same or slightly upgraded setup, it becomes stronger.

Service MSMEs can invest in digital tools

This can help them reach customers beyond the local market. For example, a repair service, small design firm, coaching class, local consultant, or B2B service provider may use digital systems to improve billing, lead tracking, customer communication, or online service delivery.

If a business takes a loan and becomes more dependent on one buyer, one machine, or one market, the risk may go up. But if the loan helps the business open a new revenue path, improve output quality, or serve more than one customer group, it can make the business more stable.

Formal Credit Can Help MSMEs Stay Prepared

Formal credit can play an important role for MSMEs in 2026. It gives businesses a structured way to borrow, repay, and build financial history.

This is important because many MSMEs still manage money informally. They may borrow from local lenders, suppliers, friends, or personal networks. In some cases, this may feel faster. But it can also create pressure because costs may not be clear, repayment terms may not be flexible, and records may not be properly maintained.

Here’s why formal borrowing helps:

Repayment History: When a business borrows through formal channels and repays on time, it creates a repayment history. Over time, this can help the business access credit more confidently.

Easier Tracking of Cash Flow: Planned borrowing can support working capital, machinery, equipment, stock purchase, seasonal demand, and order execution. It can also help MSMEs separate business expenses from personal expenses. This makes cash flow easier to understand.

Stronger Documentation: GST records, invoices, bank statements, purchase orders, stock details, and business registrations are not just paperwork. They show how the business runs and help lenders understand business activity and repayment capacity.

For MSMEs planning expansion in an uncertain year, RBI-regulated NBFCs like Protium can support business-focused credit needs. This can be useful for businesses that need funds for machinery, working capital, equipment, stock, or order-based requirements. A structured loan can help MSMEs grow without disturbing regular business expenses. It can also help business owners avoid dipping into emergency funds, delaying vendor payments, or using personal savings for business needs. But formal credit works best when the borrower is prepared. MSMEs should know why they are borrowing, how much they need, how the funds will be used, and how repayment will be managed. A loan should fit the business cycle. It should not disturb it.

———————————–

¹ Indian Industries Association, June 2026